As expected, the Fed raised short-term interest rates by a quarter point last week. Major indices responded by posting their strongest week since November 2020. This was the first rate hike since the end of 2018. Even more important, it signaled a new level of hawkishness in terms of future rate hikes as well as Quantitative Tightening to begin sometime in May. This is when the central bank will start reducing their portfolio of bonds by selling them in the open market. This is the opposite of the Fed’s strategy over the last few years when they bought bonds to help stimulate growth in the economy. This along with raising short-term interest rates will hopefully combat inflation. The challenge is tapping the brakes enough to stop inflation’s advance without throwing the economy into a recession.

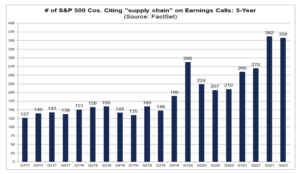

In last weeks market commentary, I posted a chart from FactSet showing a record number of companies citing inflation concerns on their most recent earnings calls with analysts. This week’s chart shows the second-highest number of companies citing “supply-chain issues” on calls with analysts. The reason this chart is just as important as last week’s chart is because they are inter-related. U.S. consumers flush with cash are finding it difficult to purchase the goods they seek. Economists had hoped this problem would have gradually corrected itself over time. When dealing with supply and distribution issues, they are finding that opening up the spigot is much more difficult than shutting it off. Some auto manufacturers are even making plans to ship cars and trucks to dealerships without some computer chip components. They plan to have buyers bring their vehicles back to the dealership in the future to have chip installations completed at no cost to the consumer. Drastic times call for drastic measures.

|

I am glad to see the market recover as strongly as it did last week. But with the war in Ukraine continuing, I expect to see more volatility for the foreseeable future. I am still bullish on the U.S. economy and stock market. If you have any questions, please contact me.

__________________________________________________________________

|

|

The Markets and Economy

Offices in Chicago, Naples & Valparaiso.

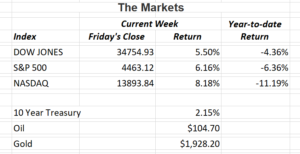

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Consult your financial professional before making any investment decision. You cannot invest directly in an index. Past performance does not guarantee future results.

Note: All figures exclude reinvested dividends (if any). Sources: Bloomberg, Dorsey Wright & Associates, Inc. and The Wall Street Journal. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

Securities offered through Triad Advisors, member FINRA/SIPC. Investment advice offered through Resources Investment Advisors, LLC, an SEC-registered investment adviser. Resources Investment Advisors. LLC and Vertical Financial Group are not affiliated with Triad Advisors.

|