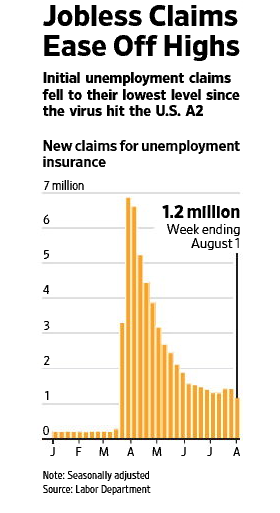

The big news last week was on the jobs front. First, on Thursday the Labor Department reported initial unemployment claims fell by a seasonally adjusted 249,000 to 1.2 million for the week ending August 1. That’s down from June’s weekly average of 1.5 million. The official unemployment rate fell to 10.2% from a peak of 15% in April. The jobless claims figure was the lowest since March when the effects of the pandemic were just starting to hit the U.S. economy. Second, on Friday the Labor Department reported hiring increased in July for the third straight month. In July, 1.8 million jobs were added.

The U.S. still has about 13 million fewer jobs than in February, the month before the coronavirus hit the U.S. economy. Unemployment remains stubbornly high according to the Labor Department as the U.S. has yet to restore half of the jobs lost during the pandemic.

The chart below, released by the Labor Department, was reprinted from the Wall Street Journal.

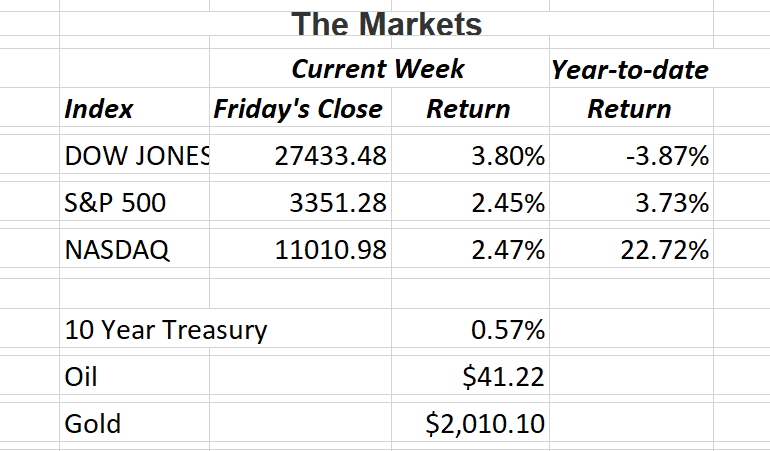

The technology sector has been one of the best performing areas in the market for several years. That’s evidenced by the tech-heavy Nasdaq rising more than 22% year-to-date.

What is driving the technology feeding frenzy? I read a recent article from Fred Alger & Company, LLC. It helps put perspective on what has been happening in the technology sector for over half a century.

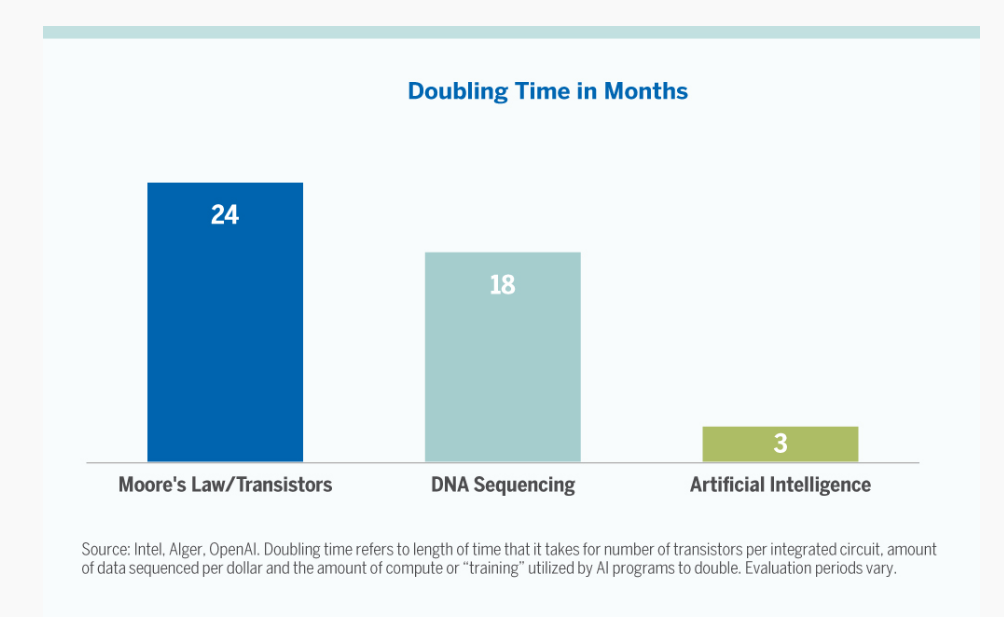

We all know how fast technology can change requiring us to deal with new layouts, designs and features as we say to ourselves…..not again? The excerpt below explains why that happens.

- Growth rates can be characterized by how long it would take to cause a doubling in the underlying data. For example, Moore’s Law stated that the number of transistors on a chip was growing so rapidly that it would cause them to double every two years. In 1965, when Moore wrote his seminal paper there had been six doublings and so there were 64 transistors on an integrated circuit. After decades of doubling, the current iPhone has some 8.5 billion transistors, ushering in productivity that we could never have imagined in the early days of integrated circuits.

- DNA sequencing is evolving even faster with the cost of a human genome declining from over $10 million 15 years ago to under $1,000 today. The amount of genetic data that can be sequenced per dollar is doubling every 18 months or so.

- The speed at which artificial intelligence (AI) programs can “train” or how much computation they can utilize is doubling approximately every 3.4 months, propelled forward by not only advances in hardware but in software as well. Given that 30 doublings is more than a billionfold increase and that AI is on pace to achieve that in less than a decade, future technology is bound to be awe inspiring.

The chart below shows the doubling time in months.

With continued advancement in technology, this sector should remain in demand for investors for several years.

The Markets and Economy

- Airlines are asking the U.S. government for more financial help to prevent massive layoffs affecting tens of thousands of workers. Airlines received $25 billion in aid under the broad economic stimulus package passed in March. The layoff restrictions in that package expire on October 1. What looked like the beginning of a rebound earlier this summer flatlined as coronavirus cases surged, triggering a new wave of travel restrictions. Corporate officials are working closely with union leadership to press the government for increased assistance until next March when a vaccine is expected to be available.

- After setting a target inflation rate of around 2% for over three decades, the Federal Reserve is expected to announce plans to abandon its strategy of preemptively raising interest rates to head off higher inflation. Fed officials would take a more relaxed view by allowing periods in which inflation would run slightly above the central bank’s 2% target, to make up for past episodes in which inflation ran below the target.

- According to the U.S. Census Bureau there were 40.8 million households that were renters. That represents 32% of the 126.8 million total households. A July survey estimates that 23.6 million of that 40.8 million (58%) fear they have “no to slight” chance of being able to pay their rent in August.

- Since cutting short-term interest rates to near zero on 3/15/20, the Fed has purchased $1.7 trillion of treasuries through Wednesday 7/29/20. The Fed now owns $4.3 trillion of U.S. government debt or 25% of the total Treasury securities outstanding.

- The U.S. and China have agreed to high-level talks on August 15 to asses Beijing’s compliance with the bilateral trade agreement signed early this year. The trade agreement is one of the few avenues for the two superpowers to engage on matters of mutual concern. Relations have deteriorated significantly this year as the Trump administration hammers Beijing over concealing the effects, timing and source of the coronavirus, the treatment of Uighurs in western China and the crack down on liberties in Hong Kong.

- As the White House and Congress remain at odds over another package of enhanced unemployment benefits, many economists are expecting a sharp drop-off in household spending. More than 12 million people were receiving benefits that ended on July 31. Some analysts believe spending could fall 4.3% in August.

- The beginnings of an economic recovery in the U.S. saw June’s imports and exports increase for the first time in six months. While trade rebounded, it is still far below where it was in February. Economists are concerned the recent resurgence in Covid-19 cases in the U.S. and other countries could reverse the gains.

Offices in Chicago, Kansas City, St. Louis, Naples & Valparaiso.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Consult your financial professional before making any investment decision. You cannot invest directly in an index. Past performance does not guarantee future results.

Note: All figures exclude reinvested dividends (if any). Sources: Bloomberg, Dorsey Wright & Associates, Inc. and The Wall Street Journal. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

Securities offered through Triad Advisors, member FINRA/SIPC. Investment advice offered through Resources Investment Advisors, LLC, an SEC-registered investment adviser. Resources Investment Advisors. LLC and Vertical Financial Group are not affiliated with Triad Advisors.