It was another volatile week on Wall Street as the stock market tried to make sense of what was already known; the Fed will begin raising interest rates at their March meeting. While many investors are worried about the old saying: “As goes January, so goes the year,” there’s good reason to expect a different outcome for 2022.

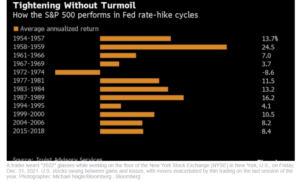

U.S. stocks have historically performed well during periods when the Fed raised interest rates. This is because a growing economy tends to support corporate profit growth and the stock market. In fact, stocks have risen at an average annualized rate of 9% during the 12 Fed rate hike cycles since the 1950’s. It has also delivered positive returns in 11 of those instances. The one exception was during the 1972-1974 period which coincided with the 1973-1975 recession.

Analysts don’t think lingering concerns about tighter monetary policy or the spread of Covid-19 will prevent the broader market from notching another positive year. According to Bloomberg, on average, analysts project that the S&P 500 will finish 2022 at 4,982, 11% above last Friday’s close. The index surged nearly 27% in 2021 – it’s third straight year of double-digit returns.

The chart below from BNN Bloomberg shows how the stock market has fared during previous Fed rate hikes.

|

In the face of recent volatility, I still remain bullish on the stock market. If you have any questions, please contact me.

|

|

The Markets and Economy

Offices in Chicago, Kansas City, St. Louis, Naples & Valparaiso.

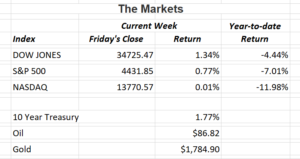

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is an unmanaged, market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System.

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

Consult your financial professional before making any investment decision. You cannot invest directly in an index. Past performance does not guarantee future results.

Note: All figures exclude reinvested dividends (if any). Sources: Bloomberg, Dorsey Wright & Associates, Inc. and The Wall Street Journal. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly.

Securities offered through Triad Advisors, member FINRA/SIPC. Investment advice offered through Resources Investment Advisors, LLC, an SEC-registered investment adviser. Resources Investment Advisors. LLC and Vertical Financial Group are not affiliated with Triad Advisors.

|